What is invoice factoring: What is invoice factoring and how does it work?

In some industries, offering a longer payback period is part of a larger negotiation strategy for getting the best deals. These are just a few of the reasons why many small businesses holding outstanding invoices turn to invoice factoring as a strategy for reducing their cash flow gap. You may be thinking, “What is invoice factoring—and how can it be beneficial for my business?

Bankrate.com is an independent, advertising-supported publisher and comparison service. We are compensated in exchange for placement of sponsored products and, services, or by you clicking on certain links posted on our site. Therefore, this compensation may impact how, where and in what order products appear within listing categories, except where prohibited by law for our mortgage, home equity and other home lending products. Other factors, such as our own proprietary website rules and whether a product is offered in your area or at your self-selected credit score range can also impact how and where products appear on this site.

Non-recourse factoring

Since your credit score plays a key role in the viability of your business, it’s important to keep a watchful eye on this number. At the very least, get a free credit report each year and make sure the information is both correct and current. A traditional, high-interest bank loan can be very expensive, not to mention the immediate debt incurred with obtaining one. We believe everyone should be able to make financial decisions with confidence. Our experts have been helping you master your money for over four decades. We continually strive to provide consumers with the expert advice and tools needed to succeed throughout life’s financial journey.

- As you might imagine, it’s very expensive and difficult to get out of this situation once you’re in it.

- Confidential factoring is a type of invoice factoring where your customers are never made aware that they’re dealing with a factoring business.

- To finance slow-paying accounts receivable or to meet short-term liquidity, businesses may opt to finance their invoices.

- When choosing a factor, you should also think about the amount and frequency of invoices you want to sell.

- With “spot” factoring, a company can sell and assign a single, individual invoice to a factor.

Trusted by over 70,000 small businesses across the U.S., Fundbox is an example of a company that can help across multiple industries. We have a reputation of excellent customer support and satisfaction, with a TrustScore of 9.7 out of 10 and an overall rating of “Excellent” on TrustPilot, and an A+ rating with the Better Business Bureau. On the customer support side, you’ll probably want to ask the company about its customer support, since your clients will be directly interacting with them. Find out how they will interact with your clients and whether the customer experience will be acceptable for your valuable clients.

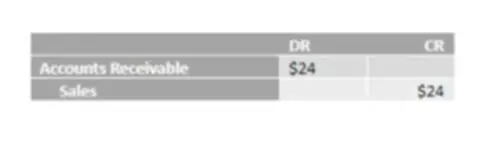

Invoice factoring example

Instead of working with banks or lenders, small business owners can work with a third party called a factoring company (also simply known as a “factor”) to access funds by “factoring” outstanding invoices. Invoice factoring is a financing plan specifically designed for businesses that issue invoices with net terms, usually between 30 to 90 days. With invoice factoring, businesses can sell their unpaid invoices to get access to extra funding quickly. You may have heard of invoice factoring or invoice discounting, but with both you access funds from an unpaid invoice. With invoice factoring, you sell your unpaid invoices to the factoring company and they collect payment directly from your customers. You also likely will receive 60-95% of the invoice value, not the entire amount.

This guide will answer all of your questions about invoice factoring, helping you determine if it’s a good fit for your business. While there are several advantages to using factoring as a form of business financing, it also has drawbacks. These pros and cons make factoring ideal for some businesses in certain industries and a poor solution for others. Invoice financing and invoice factoring have many similarities.However, there are few key differences that are relevant to your decision of whether invoice factoring or financing is a better fit for you. Suppliers can take advantage of such programs when they are provided by their buyers.

Invoice Factoring Lets You Offer Better Payment Terms To Win More Business

While invoice financing and invoice factoring are both known to be much faster than traditional bank loans, invoice financing is usually faster than invoice factoring. Because invoice factoring involves re-assigning the receiver of your client’s bill, the company offering invoice factoring may send out a “notice of assignment” to your affected clients at this stage. The notice would inform them of your invoice factoring plan, and provide them detailed instructions on how to send future payments from invoices issued from you. When choosing a factor, you should also think about the amount and frequency of invoices you want to sell. Many invoice factoring agreements require a regular, recurring arrangement.

- This is good for companies, but usually bad for factors who have already put in so much work and time to work with you through the application process.

- We believe everyone should be able to make financial decisions with confidence.

- Invoice factoring is a form of alternative financing that involves selling your outstanding invoices to a third party (factoring company) in exchange for cash up front.

Try using one of these top accounting and invoice software solutions. With NetSuite, you go live in a predictable timeframe — smart, stepped implementations begin with sales and span the entire customer lifecycle, so there’s continuity from sales to services to support. Always transparent, always fair, Triumph Business Capital offers options that match each client’s financing needs without — most importantly — incurring debt. Invoice factoring can take the stress out of meeting all your first-of-the-month commitments.

Ready to Learn More?

Factoring also makes it easier for business owners with questionable credit to get funding, because the owner’s credit isn’t really important – it’s their clients’ creditworthiness that matters. The main cost of invoice factoring is the so-called discount rate on the invoice. This is typically between 2% and 5% of the invoice’s total value, though the rate can be outside this range depending on the volume of business and the risk the factoring company is taking. In addition, the discount rate may be influenced by how many alternative sources of financing a company has at its disposal. Factoring alleviates cash flow concerns during a slow period, especially for companies with few resources and slow-paying customers. Just about every small-business owner knows what it’s like to lie awake at night wondering whether they’re going to be able to make their payroll or cover some other critical business expense.

Allows less control over certain customer interactions and impressions.

In other instances, they may adopt other methods to secure early payment on their invoices. While not all factors are entirely transparent with their pricing, Triumph Business Capital believes in being as transparent as possible, from the initial conversation through the funding process. The cost of paying for your invoices in advance can vary anywhere from 1.5–5% of the invoice value each month. This wide disparity is yet another reason to check with your factor before jumping into a relationship.