How to Claim CCA on a Business Vehicle

So you don’t have to claim the whole amount of CCA you are able to deduct in any given year. An item is recorded on a company’s books as a fixed asset at the time of purchase if it will bring value to the company over a number of years.

Business vehicles in Canada can be written off at tax time using Form T2125, Statement of Business or Professional Activities. This expense can be claimed by calculating theCapital Cost Allowance(CCA) on yourCanadianincome taxreturn. You would add this recaptured amount to your taxable income when preparing your tax return. Recapture may happen if upon selling the property the proceeds from the sale exceed the remaining undepreciated capital cost. Your undepreciated capital cost is the capital cost of all your depreciable property in the class subtracted from the allowance you claimed in prior years.

It is expected that the fixtures will have no salvage value at the end of their useful life of 10 years. Under the straight-line method, the 10-year life means the asset’s annual depreciation will be 10% of the asset’s cost.

How do you calculate half year convention?

The half-year convention is used to calculate depreciation for tax purposes, and states that a fixed asset is assumed to have been in service for one-half of its first year, irrespective of the actual purchase date. The remaining half-year of depreciation is deducted from earnings in the final year of depreciation.

The half-year convention extends the number of years the asset is depreciated, but the extension provides a more accurate matching of expenses to revenues. If you are a sole proprietor or a member of a partnership, you can claim the CCA on line 9936 ofForm T2125.

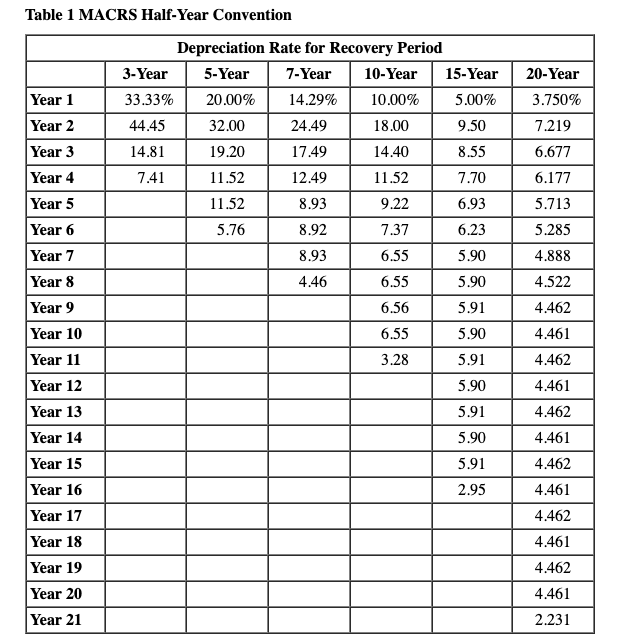

The mid-quarter convention is required by the Internal Revenue Service for tax reporting purposes if at least 40% of the cost basis of all tangible personal property acquired in a year occurs in the fourth quarter of the year. Property that is both acquired and disposed of in the same year is exempt from this requirement, as is residential rental property, nonresidential real property, and any property not being depreciated with MACRS depreciation rates. The third, the “mid-quarter convention,” assumes that all property placed into service, or disposed of, during any quarter of a taxable year was placed into service, or disposed of, at the midpoint of that quarter.

Over the life of the property, the rate is applied against the remaining balance. In applying the 40% mid quarter convention rule, you do not count residential rental property, nonresidential realty, and assets that were placed in service and disposed of during the same year. Let’s assume that a retailer purchases fixtures on January 1 at a cost of $100,000.

The double declining balance method of depreciation, also known as the 200% declining balance method of depreciation, is a form of accelerated depreciation. This means that compared to the straight-line method, the depreciation expense will be faster in the early years of the asset’s life but slower in the later years. However, the total amount of depreciation expense during the life of the assets will be the same. There’s no harm in doing this as long as each version clearly states the assumptions made and as long as all tax-related submissions are consistent. Accounting departments often evaluate balance sheets using different methods of depreciation to determine which is the most advantageous for the business based on the magnitude of the asset in question.

Half-Year Convention For Depreciation

The Canada Revenue Agency has specific requirements for claiming the CCA on Rental Property. A fully depreciated asset is a property, plant or piece of equipment (PP&E) which, for accounting purposes, is worth only its salvage value. Whenever an asset is capitalized, its cost is depreciated over several years according to a depreciation schedule. Theoretically, this provides a more accurate estimate of the true expenses of maintaining the company’s operations each year. Depreciable properties are those that have been worn out from use over the years, such as automobiles and farm and business equipment.

Alternatively, you might be allowed to take a “terminal loss” deduction from your income. Terminal loss is when you don’t have any depreciable property in the class at the end of the year, but you have an outstanding CCA amount that you have not claimed. “Upon sale, any profit you earned on the rental property over and above your initial cost will be treated as a capital gain. Capital gains are taxed at 50 percent of the gain, whereas recapture is 100 percent taxable,” says Lior Zehtser.

- Business vehicles in Canada can be written off at tax time using Form T2125, Statement of Business or Professional Activities.

- This expense can be claimed by calculating theCapital Cost Allowance(CCA) on yourCanadianincome taxreturn.

- You would add this recaptured amount to your taxable income when preparing your tax return.

Owning a rental property provides not only income, but also deductions you can take at tax time. This includes rental expenses, such as homeowner’s insurance, property taxes, maintenance fees, advertising, mortgage interest, utility costs and property management fees. You also may qualify for the capital cost allowance, or CCA, which is depreciation that can be claimed on your return.

This means you can write off the capital cost of the property including the purchase price, legal fees associated with the purchase of the property and cost of equipment and furniture that comes with renting a building. If you rent out part of your principal residence, you should exercise caution before making a CCA claim for your home. An asset can reach full depreciation when its useful life expires or if an impairment charge is incurred against the original cost, though this is less common. If a company takes a full impairment charge against the asset, the asset immediately becomes fully depreciated, leaving only its salvage value (also known as terminal value or residual value). For the most part, use the declining balance method to calculate your CCA, as it is the most common one.

How does half year rule work?

Example of the Half-Year Convention The straight-line method of depreciation expense is calculated by dividing the difference between the cost of the truck and the salvage value by the expected life of the truck. In this example, the calculation is $105,000 minus $5,000 divided by 10 years, or $10,000 per year.

Example of the Half-Year Convention

If the company purchases the truck in July rather than January, however, it is more accurate to use the half-year convention to better align the cost of the equipment with the time period in which the truck provides value. Instead of depreciating the full $10,000 in year one, the half-year convention expenses half of the calculated depreciation expense, or $5,000 in year one. In years two through 10, the company expenses $10,000, and then in year 11, the company expenses the final $5,000.

How does proration affect asset depreciation?

Canadian corporations can also claim the CCA on vehicles they’ve purchased for business use in the appropriate section of the T2 corporate income tax return. The CAA calculation is the same for corporations, sole proprietors and partners, and the same CCA classes and rules apply.

Depreciation allows a company to expense a portion of the cost of an asset in each of the years of the asset’s useful life. The company will then keep track of the book value of the asset by subtracting the accumulated depreciation from the asset’s historical cost.

(§ 168(d)(C)) Section 168(d) tells a taxpayer when it is appropriate to use the mid-quarter convention. Your Capital Cost Allowance claim is like a running tally from year to year.

Under thedouble declining balance method the 10% straight line rate is doubled to 20%. However, the 20% is multiplied times the fixture’s book value at the beginning of the year instead of the fixture’s original cost. The units of production depreciation method is used when the lifetime of an asset is defined in hours of operation, units produced or another iteration affected not just by time but by usage of the asset. In this case, depreciation is calculated based on the production rates the company expects to manufacture while the asset is in use. To determine the amount, you would likely use the “declining balance method.” In this case, your CCA amount is based on any allowance claimed in prior years subtracted from the capital cost of the property.

You can claim any amount of your allowance for the year—you do not have to the take the full amount all at once. For example, you might want to hold off on claiming your CCA if you don’t owe any taxes for the year, since taking the allowance lowers the amount you’re entitled to in upcoming years. Capital Cost Allowance (CCA) is the tax deduction for depreciable property, property such as furniture, equipment, computers or even buildings that wear out over time (depreciate).