Income Statement vs. P&L

Also known as the profit and loss statement or the statement of revenue and expense, the income statement primarily focuses on the company’s revenues and expenses during a particular period. A balance sheetis a summary of the financial balances of a company, while a cash flow statement shows how the changes in the balance sheet accounts–and income on the income statement–affect a company’s cash position.

The cash activities are instead, recorded on the cash flow statement. The balance sheet and cash flow statement are two of the three financial statements that companies issue to report their financial performance. The financial statements are used by investors, market analysts, and creditors to evaluate a company’s financial health and earnings potential. While the balance sheet shows what a company owns and owes, the cash flow statement records the cash activities for the period.

Some refer to the P&L statement as a statement of profit and loss, income statement, statement of operations, statement of financial results or income, earnings statement or expense statement. Financial statements are written records that convey the business activities and the financial performance of a company. Financial statements include the balance sheet, income statement, and cash flow statement. The balance sheet shows a snapshot of the assets and liabilities for the period, but it does not show company’s activity during the period, such as revenue, expenses, nor the amount of cash spent.

Regulatory groups, standards boards, and tax authorities allow or require companies to use conventions such as depreciation expense, cost allocation, and accrual accounting on the Income statement. Direct reports of actual cash flow gains and losses for the period appear on another reporting instrument, the Statement of changes in financial position (or Cash flow statement).

The P&L statement shows a company’s ability to generate sales, manage expenses, and create profits. Cash purchases are recorded more directly in the cash flow statement than in theincome statement. In fact, specific cash outflow events do not appear on the income statement at all.

The income statement reflects a company’s performance over a period of time. This is in contrast to the balance sheet, which represents a single moment in time. Income statements show how much profit a business generated during a specific reporting period and the amount of expenses incurred while earning revenue. The last line of the income statement, net income tells you exactly how much profit the company made or exactly how big of a loss it suffered. Net income may differ from operating income because of non-operating items, or those not related to the company’s core business.

An income statement is one of the three (along with balance sheet and statement of cash flows) major financial statements that reports a company’s financial performance over a specific accounting period. Although you haven’t earned deferred revenue yet, it’s still cash that you can spend. In accrual accounting, the cash flow statement exists to reconcile the difference between profits you report on the income statement and the cash balance that winds up on your balance sheet.

For example, outstanding credit sales get subtracted, since they produced revenue (and profit) but not yet any cash flow. Deferred revenue gets added in at this point because it produced cash flow without revenue (or profit). Net Income is a key line item, not only in the income statement, but in all three core financial statements. While it is arrived at through the income statement, the net profit is also used in both the balance sheet and the cash flow statement. A profit and loss statement (P&L), or income statement or statement of operations, is a financial report that provides a summary of a company’s revenues, expenses, and profits/losses over a given period of time.

Net income or loss is represented on the income statement and statement of owner’s equity in year-end or quarterly financial statements. Note by the way, that reports of “Income,” “Revenues,” and “Expenses” do not necessarily represent real cash inflows or outflows. Not all of these signal the presence of “cash flow” for the following reason.

How do you prepare an income statement worksheet?

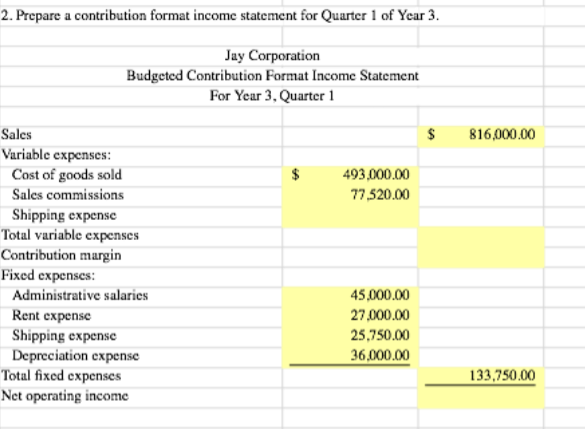

The income statement calculates the net income of a company by subtracting total expenses from total income. For example annual statements use revenues and expenses over a 12-month period, while quarterly statements focus on revenues and expenses incurred during a 3-month period.

How to Write an Income Statement

One can infer whether a company’s efforts in reducing the cost of sales helped it improve profits over time, or whether the management managed to keep a tab on operating expenses without compromising on profitability. Net income (the “bottom line”) is the result after all revenues and expenses have been accounted for.

- Also known as the profit and loss statement or the statement of revenue and expense, the income statement primarily focuses on the company’s revenues and expenses during a particular period.

- A balance sheetis a summary of the financial balances of a company, while a cash flow statement shows how the changes in the balance sheet accounts–and income on the income statement–affect a company’s cash position.

Calculate Net Income

Creditors may find limited use of income statements as they are more concerned about a company’s future cash flows, instead of its past profitability. Research analysts use the income statement to compare year-on-year and quarter-on-quarter performance.

How do you create an income statement?

To prepare an income statement generate a trial balance report, calculate your revenue, determine the cost of goods sold, calculate the gross margin, include operating expenses, calculate your income, include income taxes, calculate net income and lastly finalize your income statement with business details and the

Rather, different items on the operating section of a company’s income statement are affected by the balance of cash purchases, credit purchases and other previously recorded transactions. One of the limiting features of the income statement is it does not show when revenue is collected or when expenses are paid. The income statement tells you how much money a company has brought in (its revenues), how much it has spent (its expenses), and the difference between the two (its profit). The income statement shows a company’s revenues and expenses over a specific time frame such as three months or a year.

It tracks all cash coming into and going out of the company, regardless of whether the transactions have been officially booked yet. In the most common format for a cash flow statement, the company starts with the profit reported on the income statement, then adds and subtracts items based on whether they produced real cash flow.

Revenues, or income, are amounts earned from primary business activities, like product sales, or other financial gains. The bottom line of the income statement is the net profit or loss, depending on if your revenues are more or less than your expenses. For example, a company’s revenues may grow, but its expenses might grow at a faster rate.

The P&L statement is one of three financial statements every public company issues quarterly and annually, along with the balance sheet and the cash flow statement. It is often the most popular and common financial statement in a business plan as it quickly shows how much profit or loss was generated by a business.

Calculate Your Revenue

This statement contains the information you’ll most often see mentioned in the press or in financial reports–figures such as total revenue, net income, or earnings per share. Your net income or net loss equals your total revenues minus your total expenses for an accounting period.

Calculate Your Income

The balance sheet, on the other hand, is a snapshot, showing what the company owns and owes at a single moment. It is important to compare the income statement with the cash flow statement since, under the accrual method of accounting, a company can log revenues and expenses before cash changes hands. The profit and loss (P&L) statement is a financial statement that summarizes the revenues, costs, and expenses incurred during a specified period, usually a fiscal quarter or year. These records provide information about a company’s ability or inability to generate profit by increasing revenue, reducing costs, or both.

And, net income from operations—before taxes, before gains and losses from financial and extraordinary items—is named, not surprisingly, Operating Income or operating profit. One can use the income statement to calculate several metrics, including the gross profit margin, the operating profit margin, the net profit margin and the operating ratio. Together with the balance sheet and cash flow statement, the income statement provides an in-depth look at a company’s financial performance.

In other words, a company’s cash flow statement measures the flow of cash in and out of a business, while a company’s balance sheet measures its assets, liabilities, and owners’ equity. The cash flow statement summarizes your incoming and outgoing money from operations, investing, and financing. The income statement, like the cash flow statement, shows changes in accounts over a set period.

ottom line Net income is one measure of the company’s financial performance for the period. However, the Income statement contains other performance metrics as well. The difference between Net sales revenues and Cost of goods sold is called Gross profit, for instance.