Is a house an asset or liability?

The non-cash working capital for the Gap in January 2001 can be estimated. Current assets are not necessarily very liquid, and so may not be available for use in paying down short-term liabilities. In particular, inventory may only be convertible to cash at a steep discount, if at all.

Current assets listed on a company’s balance sheet include cash, accounts receivable, inventory and other assets that are expected to be liquidated or turned into cash in less than one year. Current liabilities include accounts payable, wages, taxes payable, and the current portion of long-term debt. Companies with high amounts of working capital possess sufficient liquid funds needed to meet their short-term obligations.

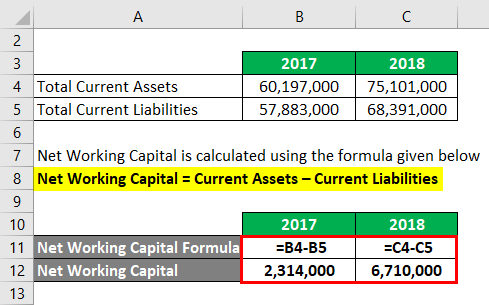

Net Working Capital Formula

From a strict accounting standpoint, basic working capital is current assets (cash, inventory, a/r) minus current liabilities (a/p, short term debt). This essentially represents a company’s liquidity, or ability to meet short term demands. Net working capital measures a company’s ability to meet its current financial obligations. When a company has a positive net working capital, it means that it has enough short-term assets to finance to pay its short-term debts and even invest in its growth.

Working capital, also called “net working capital,” is a liquidity metric used in corporate finance to assess a business’ operational efficiency. It is calculated by subtracting a company’s current liabilities from its current assets. Current assets are assets that a company reasonably expects to convert into cash within one year.

In this scenario, a company may turn to traditional financing options to bolster its working capital, such as loans, lines of credit or cash advances. In addition, a company may also raise capital through the selling of equity, selling of invoices, (invoice factoring) or arranging inventory advances (trade credit).

If a company’s current assets do not exceed its current liabilities, then it may have trouble growing or paying back creditors, or even go bankrupt. Net operating working capital is a measure of a company’s liquidity and refers to the difference between operating current assets and operating current liabilities. In many cases these calculations are the same and are derived from company cash plus accounts receivable plus inventories, less accounts payable and less accrued expenses. Regardless of a company’s size or industry sector, working capital is an important metric in assessing the long-term financial health of the business. The level of working capital available to an organization can be measured by comparing its current assets against current liabilities.

Working capital serves as a metric for how efficiently a company is operating and how financially stable it is in the short-term. The working capital ratio, which divides current assets by current liabilities, indicates whether a company has adequate cash flow to cover short-term debts and expenses. Working capital is a measure of a company’s liquidity, operational efficiency and its short-term financial health. If a company has substantial positive working capital, then it should have the potential to invest and grow.

Why Net working capital is important?

Working capital is the amount of a company’s current assets minus the amount of its current liabilities. Net working capital equals a company’s total current assets minus its total current liabilities.

Changes to Net Working Capital

Current assets can include cash, accounts receivable, and inventory, among others. Current liabilities are a company’s bills and other obligations that are due within one year.

A managerial accounting strategy focusing on maintaining efficient levels of both components of working capital, current assets, and current liabilities, in respect to each other. Working capital management ensures a company has sufficient cash flow in order to meet its short-term debt obligations and operating expenses.

Generally, the larger your net working capital balance is, the more likely it is that your company can cover its current obligations. It is a measure of a company’s liquidity and its ability to meet short-term obligations, as well as fund operations of the business. The ideal position is to have more current assets than current liabilities, and thus have a positive net working capital balance. Current liabilities are financial obligations of a business entity that are due and payable within a year. A liability occurs when a company has undergone a transaction that has generated an expectation for a future outflow of cash or other economic resources.

Liabilities are considered current liabilities if the debts or obligations are due within one year. Working capital is the difference between a business’ current assets and current liabilities or debts.

- However, the amount of net working capital alone does not assure a company of the liquidity necessary to pay its current liabilities when they come due.

- Net working capital is often cited as one of the indicators of a company’s liquidity.

- Not having sufficient cash to pay employees, suppliers and other creditors may lead to serious problems.

Companies can increase their net working capital by increasing their current assets and decreasing their short-term liabilities. Current liabilities are short-term financial obligations due in 1 year or less. Current liabilities usually include short-term loans, lines of credit, accounts payable, accrued liabilities, and other debts such as credit cards, trade debts, and vendor notes.

As a specialty retailer, the Gap has substantial inventory and working capital needs. At the end of the 2000 financial year (which concluded January 2001), the Gap reported $1,904 million in inventory and $335 million in other non-cash current assets. At the same time, the accounts payable amounted to $1,067 million and other non-interest bearing current liabilities of $702 million.

Current portions of long-term debt like commercial real estate loans and small business loans are also considered current liabilities. Net working capital is the difference between a business’s current assets and its current liabilities. Net working capital is calculated using line items from a business’s balance sheet.

A company’s liabilities are any financial debt or obligations that a company is responsible for due to its business operations. Liabilities often include “payable” in their account title on the balance sheet. Examples of liabilities are notes payable, accounts payable, salaries payable, wages payable and income taxes payable.

If the figure is substantially negative, then the business may not have sufficient funds available to pay for its current liabilities, and may be in danger of bankruptcy. The net working capital figure is more informative when tracked on a trend line, since this may show a gradual improvement or decline in the net amount of working capital over time.

What is the difference between net working capital and working capital?

Net working capital (NWC) is the difference between a company’s current assets and current liabilities. A positive net working capital indicates a company has sufficient funds to meet its current financial obligations and invest in other activities.

Further, accounts receivable may not be collectible in the short term, especially if credit terms are excessively long. This is a particular problem when large customers have considerable negotiating power over the business, and so can deliberately delay their payments. If the net working capital figure is substantially positive, it indicates that the short-term funds available from current assets are more than adequate to pay for current liabilities as they come due for payment.

This tells the business the short-term, liquid assets remaining after short-term liabilities have been paid off. A company can be endowed with assets and profitability but may fall short of liquidity if its assets cannot be readily converted into cash. Positive working capital is required to ensure that a firm is able to continue its operations and that it has sufficient funds to satisfy both maturing short-term debt and upcoming operational expenses. The management of working capital involves managing inventories, accounts receivable and payable, and cash.

Remember to exclude cash under current assets and to exclude any current portions of debt from current liabilities. For clarity and consistency, lay out the accounts in the order they appear in the balance sheet. If a company uses its cash to pay for a new vehicle or to expand one of its buildings, the company’s current assets will decrease with no change to current liabilities. Current assets include a company’s liquid cash as well as other assets that can be converted to cash within one year or less. Some examples of current assets include money in checking accounts, inventory, supplies, equipment, and temporary investments.

A company with negative working capital (more liabilities than assets) is generally seen as being in financial risk for increased debt (which may lead to bankruptcy). If a company has negative working capital, it may have trouble paying back its short-term debt.

Not having sufficient cash to pay employees, suppliers and other creditors may lead to serious problems. To calculate the working capital, compare a company’s current assets to its current liabilities.

Current Liabilities

Net working capital is often cited as one of the indicators of a company’s liquidity. However, the amount of net working capital alone does not assure a company of the liquidity necessary to pay its current liabilities when they come due.