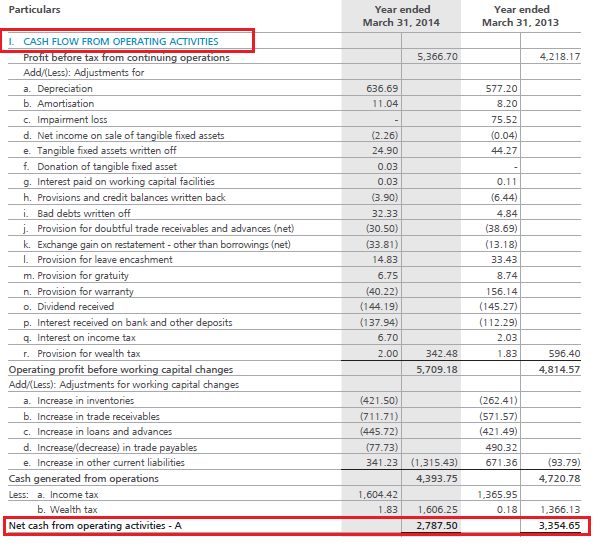

Operating Cash Flow Ratio

Any time your company spends or gains money by investing, you report it on the cash flow statement. Add up any money received from the sale of assets, paying back loans or the sale of stocks and bonds.

What Is Cash Flow from Investing Activities?

Cash flow from investing activities is the net change in a company’s investment gains or losses during the reporting period, as well as the change resulting from any purchase or sale of fixed assets. If a company reports a negative amount of cash flow from investing activities, that’s a good clue that the business is investing in capital assets, which means in the future, you can expect their earnings to grow.

It is separate from the sections on investing and financing activities. Cash flow from investing activities is a line item on a business’s cash flow statement, which is one of the major financial statements that companies prepare.

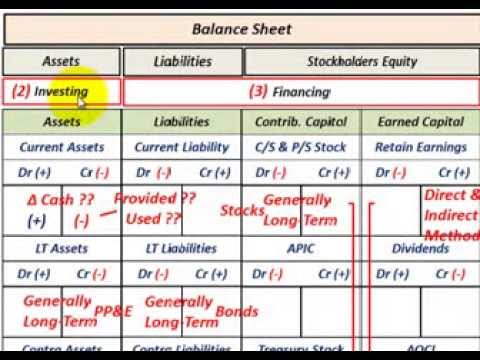

The company’s balance sheet and income statement help round out the picture of its financial health. Investing activities are one of the main categories of net cash activities that businesses report on the cash flow statement. Investing activities in accounting refers to the purchase and sale of long-term assets and other business investments, within a specific reporting period.

That’s especially true in capital-driven industries like manufacturing, which require big investments in fixed assets to grow their businesses. Investing activities encompass disposal and purchase of property, plant and equipment and other non-current assets such as investment property and machinery. Cash flow from investing activities is one of the sections on the cash flow statement that reports how much cash has been generated or spent from various investment-related activities in a specific period. Investing activities include purchases of physical assets, investments in securities, or the sale of securities or assets. The Cash Flow Statement provides the cash flow of the operating, investing, and financing activities to disclose the entire cash flow in a consolidated statement.

Operational cash flow shows how much money you generate from your company’s core purpose. The cash flow statement separates operational and investment income because income from profitable investments could hide that your company doesn’t get much revenue the regular way.

This equals dividends paid during the year, which is found on the cash flow statement under financing activities. Financing and investment activities are excluded because the purpose of the operating cash flow is to segregate and evaluate the health of the normal operations or core business. Operating cash flow (OCF) is one of the most important numbers in a company’s accounts. It reflects the amount of cash that a business produces solely from its core business operations.

Corporate Cash Flow: Understanding the Essentials

Any change in the balances of each line item of working capital from one period to another will affect a firm’s cash flows. For example, if a company’s accounts receivable increase at the end of the year, this means that the firm collected less money from its customers than it recorded in sales during the same year on its income statement. This is a negative event for cash flow and may contribute to the “Net changes in current assets and current liabilities” on the firm’s cash flow statement to be negative. On the flip side, if accounts payable were also to increase, it means a firm is able to pay its suppliers more slowly, which is a positive for cash flow. Working capital is calculated as current assets minus current liabilities on the balance sheet (see Lesson 302).

Just as the name suggests, working capital is the money that the business needs to “work.” Therefore, any cash used in or provided by working capital is included in the “cash flows from operating activities” section. It’s important for accountants, financial analysts, and investors to understand what makes up this section of the cash flow statement and what financing activities include.

Without a positive cash flow from operations a company cannot remain solvent in the long run. A negative operating cash flow would mean the company could not continue to pay its bills without borrowing money (financing activity) or raising additional capital (investment activity).

Subtract money paid out to buy assets, make loans or buy stocks and bonds. The total is the figure that gets reported on your cash flow statement.

A business’s reported investing activities give insights into the total investment gains and losses it experienced during a defined period. Investing activities are a crucial component of a company’s cash flow statement, which reports the cash that’s earned and spent over a certain period of time. The cash flow statement is useful in measuring how effectively a company manages its cash from operating activities, or day-to-day operating expenses, and its financing activities, how debt and equity is managed. Investors examine a company’s cash flow from operating activities separately from the other two components of cash flow to see where a company is really getting its money. Operating activities are the functions of a business directly related to providing its goods and/or services to the market.

- Operational cash flow shows how much money you generate from your company’s core purpose.

- If you’ve made significant expenditures for fixed assets, the opposite could happen, and it would make your cash flow from operations look worse than it is.

If you’ve made significant expenditures for fixed assets, the opposite could happen, and it would make your cash flow from operations look worse than it is. Cash flow from investing activities is critical because it shows you have resources, even if cash flow from operations is low. If you’re in an industry that requires substantial investment in fixed assets, negative cash flow from investments can be a good sign that shows you’re investing in your business’s equipment.

Since this is the section of the statement of cash flows that indicates how a company funds its operations, it generally includes changes in all accounts related to debt and equity. Cash flow from investing activities includes any inflows or outflows of cash from a company’s long-term investments. The balance sheet provides an overview of a company’s assets, liabilities, and owner’s equity as of a specific date. The income statement provides an overview of company revenues and expenses during a period.

How Do the Balance Sheet and Cash Flow Statement Differ?

Which is an example of a cash flow from a financing activity?

Items that may be included in the investing activities line item include the following: Purchase of fixed assets (negative cash flow) Sale of fixed assets (positive cash flow) Purchase of investment instruments, such as stocks and bonds (negative cash flow)

The Operating Cash Flow Calculation will provide the analyst with the most important metric for evaluating the health of a company’s core business operations. The Operating Cash Flow Calculation is operating income before depreciation minus taxes and adjusted for changes in working capital. Financing activities (dividends, issuance/purchase of common stock, issuance/purchase of debt securities) and investing activities (i.e. Operating cash flow is important because it provides the analyst insight into the health of the core business or operations of the company.

The cash flow statement bridges the gap between the income statement and the balance sheet by showing how much cash is generated or spent on operating, investing, and financing activities for a specific period. To summarize other linkages between a firm’s balance sheet and cash flow from financing activities, changes in long-term debt can be found on the balance sheet, as well as notes to the financial statements. Dividends paid can be calculated from taking the beginning balance of retained earnings from the balance sheet, adding net income, and subtracting out the ending value of retained earnings on the balance sheet.

These are the company’s core business activities, such as manufacturing, distributing, marketing, and selling a product or service. Operating activities will generally provide the majority of a company’s cash flow and largely determine whether it is profitable. Some common operating activities include cash receipts from goods sold, payments to employees, taxes, and payments to suppliers.

What is included in cash flow from investing activities?

Examples of more common cash flow items stemming from a firm’s financing activities are: Receiving cash from issuing stock or spending cash to repurchase shares. Receiving cash from issuing debt or paying down debt. Paying cash dividends to shareholders.

Operating cash flow is intensely scrutinized by investors, as it provides vital information about the health and value of a company. If a company fails to achieve a positive OCF, the company cannot remain solvent in the long term. A negative OCF indicates that a company is not generating sufficient revenues from its core business operations, and therefore needs to generate additional positive cash flow from either financing or investment activities. Investors want to see positive cash flow because of positive income from operating activities, which are recurring, not because the company is selling off all its assets, which results in one-time gains.

What Is Cash Flow From Financing Activities?

It is particularly important in capital-heavy industries, such as manufacturing, that require large investments in fixed assets. Operating cash flow (OCF) is cash generated from normal operations of a business. Cash flows from operating activities are among the major subsections of thestatement of cash flows.