What's the Difference Between Direct vs. Indirect Costs?

BUSINESS OPERATIONS

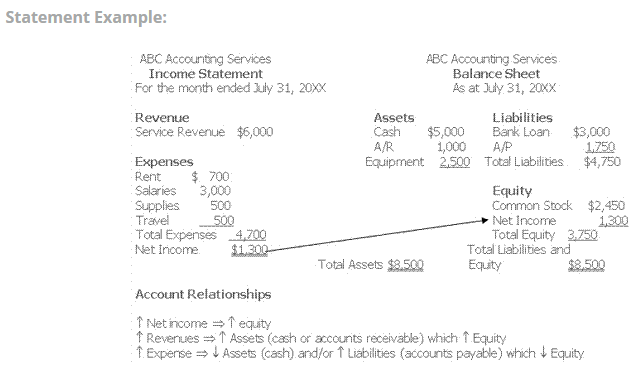

The cost of goods sold is deducted from your gross receipts to figure the gross profit for your business each year. Claiming all of your business expenses, including COGS, increases your tax deductions and decreases your business profit.

Then, as it sells the items, it expenses $1 worth of the freight charge for each one sold. If it sold 85 of them, for example, it would expense $85 of the fright charge, reducing profit by $85. The remaining $15 of the charge remains locked up in inventory until those 15 items are sold. Businesses need to track all of the costs that are directly and indirectly involved in producing their products for sale. These costs are called the cost of goods sold (COGS), and this calculation appears in the company’s profit and loss statement (P&L).

Once a business has goods in its possession, it can’t include any further freight charges in inventory cost. For example, if a company ships goods among its stores, the costs of doing so can’t be included in inventory. Instead, those costs are what accountants call selling, general and administrative expenses. Freight out, or the cost of delivering goods from the business to its customers, is also an SG&A expense.

All the machines are the same, but they have serial numbers. Under specific identification, the cost of goods sold is 10 + 12, the particular costs of machines A and C. If she uses average cost, her costs are 22 ( (10+10+12+12)/4 x 2). Thus, her profit for accounting and tax purposes may be 20, 18, or 16, depending on her inventory method. After the sales, her inventory values are either 20, 22 or 24.

And when you know your business’s gross profit, you can calculate your net income or profit, which is the amount your business earns after subtracting all expenses. Costs of materials include direct raw materials, as well as supplies and indirect materials. Carriage outwards is the shipping and handling costs incurred by a company that is shipping goods to a customer. The company may be able to bill customers for this cost; if not, then the company should charge the cost to expense in the period incurred.

Costs of selling, packing, and shipping goods to customers are treated as operating expenses related to the sale. At the start of 2009, she has no machines or parts on hand. She buys machines A and B for 10 each, and later buys machines C and D for 12 each.

COGS does not include indirect expenses, like certain overhead costs. Do not factor things like utilities, marketing expenses, or shipping fees into the cost of goods sold. When you are calculating the cost of your products, how do you handle the freight? Or do you pay it from an expense account designated for freight or shipping? Forcorporations and S corporations, the cost of goods sold is included in the corporate tax return (Form 1120) or the S corporation tax return (Form 1120-S).

Freight

Businesses that pay shipping can usually include these charges as part of inventory costs. This avoids the need to expense shipping charges for purchasing inventory items. Companies will record the expenses as an asset along with the cost paid for inventory.

What is freight in and freight out in accounting?

Freight out is the transportation cost associated with the delivery of goods from a supplier to its customers. This cost should be charged to expense as incurred and recorded within the cost of goods sold classification on the income statement.

- Businesses that pay shipping can usually include these charges as part of inventory costs.

BUSINESS PLAN

The cost of goods sold is included in Part 1 Income as part of the calculation of gross profit. GAAP provides directions for accountants needing to record shipping charges. Proper reporting depends on accounting reviewing the shipping charges for each transaction and applying GAAP to the specific situation. This ensures the company properly reports shipping charges and does not overstate revenue or understate cost of goods sold or expenses.

The shipping charges will eventually fall under the company’s cost of goods sold when they sell inventory items. This is a cost that ultimately reduces a company’s gross profit and net income. Additional costs may include freight paid to acquire the goods, customs duties, sales or use taxes not recoverable paid on materials used, and fees paid for acquisition. For U.S. income tax purposes, some of these period costs must be capitalized as part of inventory.

The accounting treatment of freight costs matters because it affects how much profit the business will show in its financial statements. Expenses reduce profit, and companies do not claim inventory costs as expenses until they actually sell the inventory. Say a company gets a shipment of 100 items, with a total freight charge of $100, or $1 per item. If the company does not include the charge in its inventory cost, then it claims an immediate SG&A expense for $100. However, if the company does include the freight in its inventory cost, it reports no immediate expenses, so there’s no reduction in profit.

When a customer receives freight and is responsible for paying the charges, it is considered freight in. If the goods are included in inventory, the expense is categorized as cost of goods sold and is reported beneath sales on the multi step profit and loss statement. On the single step statement, COGS is reported and can be analyzed, but its position on the financial statement is listed differently.

Carriage inwards is the shipping and handling costs incurred by a company that is receiving goods from suppliers. The most appropriate accounting treatment of carriage inwards is to include it in the overhead cost pool that is allocated to the goods produced in an accounting period. If this is a minor amount, it could just be charged to expense in the period incurred, with no inclusion in the overhead cost pool.

An article in “Entrepreneur” magazine points out that small and growing businesses rarely include freight in their inventory costs. Instead, they report the whole freight charge immediately as SG&A to get the maximum reduction in reported profit. While large companies want to report big profits to their shareholders, smaller ones are more concerned with limiting their tax liability. Companies pay taxes based on their profits, so the lower the reported profit, the smaller the tax bite. Keep in mind that, regardless of how its books treats freight charges, the company has already paid the full charge.

BUSINESS IDEAS

It’s also an important part of the information the company must report on its tax return. The cost of goods sold (COGS), also referred to as the cost of sales or cost of services, is how much it costs to produce your products or services. COGS include direct material and direct labor expenses that go into the production of each good or service that is sold. Cost of Goods Sold are also known as “cost of sales” or its acronym “COGS.” COGS refers to the cost of goods that are either manufactured or purchased and then sold. COGS count as a business expense and affect how much profit a company makes on its products, according to The Balance.

Thus, the cost of carriage outwards should appear in the income statement in the same reporting period as the sale transaction to which it relates. The cost of carriage outwards usually appears within the cost of goods sold section in the income statement.

Thus, depending on the accounting treatment, it may first appear in the balance sheet as an asset, and then shift to the cost of goods sold in the income statement as goods are sold. Cost of Goods Sold (COGS) is the cost of a product to a distributor, manufacturer or retailer. Sales revenue minus cost of goods sold is a business’s gross profit. Cost of goods sold is considered an expense in accounting and it can be found on a financial report called an income statement. There are two way to calculate COGS, according to Accounting Coach.